NON-CASH ASSETS – YOUR “OTHER 90%”

Scientists tell us that only about 10% of an iceberg is visible above the water’s surface. The great mass – some 90% of the iceberg is below the surface and hidden from view. Quite often, the Christian steward’s assets (or estate) are similar to an iceberg with approximately 10% in cash (liquid assets) and the remaining 90% being non-cash, non-liquid assets.

For generous stewards, this can lead to the highly frustrating, “I’d really like to give more – but I just don’t have any more money…” syndrome. Regardless of income, nearly everyone reaches the point of – “I can’t give away any more cash.”

Are there options for the giver who has reached their personal “cash limit?” Yes! For many, “the other 90%” of their financial assets holds the key to giving to their heart’s desire.

COMMON NON-CASH GENEROSITY OPTIONS

As a general rule – if the asset has an ascertainable value and is commonly bought and sold, it may be possible to use it to fulfill your generosity desires. However, some assets have complicated tax and ownership rules that make their use as a charitable gift less desirable or are prohibited.

Here is a partial list of non-cash assets that are commonly used to make generous charitable gifts.

Tangible Property – Physical property that can be moved.

Artwork, automobiles, boats, RVs, motorcycles, and collectibles such as jewelry and coins are all tangible items that can be used to make charitable gifts. Specific valuation and charitable deduction rules apply making each item more or less valuable as a gift for the giver. However, once converted to cash (or put to use by the ministry) – tangible items can be very valuable to accomplish the ministry purpose and mission.

Securities (Stocks, Bonds, Mutual Funds) – Simplest to give are those traded on a public stock exchange or market.

Example: Ralph and Marge have a significant portfolio of highly appreciated stock that is subject to equally significant capital gains tax if they sell it. Recently, they learned that using the stock for some of their giving to ministry might make good financial sense.

In a typical year, Ralph and Marge have been giving $5,000 to their favorite ministry. This year, however, rather than writing a check, they donated $5,000 in shares of appreciated stock. The ministry sold the shares providing cash to do their mission. For the ministry, the gift was virtually the same as past gifts from Ralph and Marge.

The results for Ralph and Marge, however, were important. Along with a charitable tax deduction for the fair market value of the donated stock, they also avoided the capital gains tax that would have been paid had they sold the stock. In addition, they can use the normally donated cash for any purpose they choose. And, of course, they still made their desired gift to their favorite ministry.

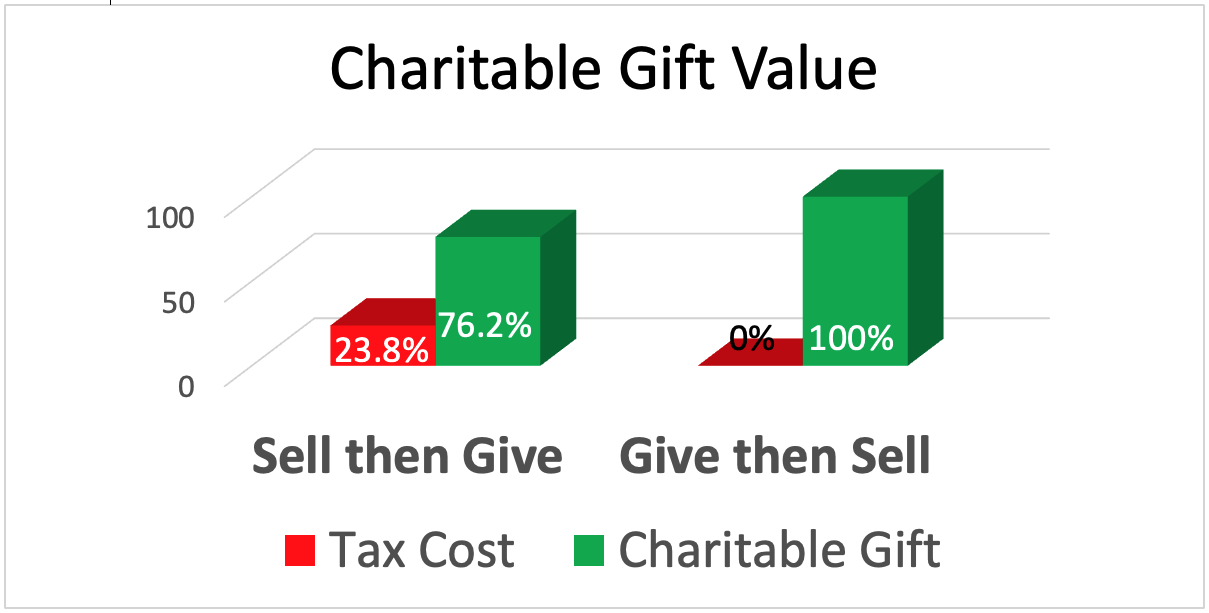

The following chart compares the value of contributing appreciated stock to charity with the result of to selling the stock and then making a gift of the after-tax cash. This illustration assumes a 23.8% combined federal and state capital gains tax rate.

Closely held securities can also be used to make charitable gifts – but may require a higher level of planning.

With all contributions of securities, it is important to consult your tax professionals to be sure you are accomplishing your generosity desires in the most cost-effective way for both you and the recipient ministry.

Individual Retirement Accounts – Commonly referred to as an IRA

Example: Ralph and Marge are in their late 70s and want to give a generous gift to their favorite ministry for the current campaign. They are doing well living on their fixed income payments and find that they really do not need the income from the required minimum distributions (RMD) they must take from their IRAs.

After learning of the qualified charitable distribution provision in the Tax Code – Ralph and Marge each instructed their IRA custodian to send a distribution equal to this year’s RMD directly to ministry to help with the campaign. While they will not receive a charitable tax deduction for the gift, they won’t have to claim the distribution as income – giving them essentially the same tax benefit.

In addition, Ralph and Marge are planning to use the qualified charitable distribution in coming years to increase their generosity. If they ever find they need the RMD (or more), they will simply not request the distribution to charity retaining the income for themselves.

Generally, if you are at least 70.5 years of age, IRAs can be excellent assets for making current gifts so long as you understand and follow the withdrawal and taxation rules carefully.

The qualified charitable distribution provision in the Tax Code allows you to have your IRA custodian send a distribution directly to your chosen ministry rather than to you. Since you don’t receive the distribution, you will not have to claim it as income. Further, the distribution can count toward your RMD for the year of the distribution.

We have prepared a helpful eBook, A Guide Charitable Giving Through Your Retirement Accounts, and you can read or download it here.

Real Estate – Buildings and Land

Example: Ralph and Marge invested in a commercial warehouse property partnership as an income-producing asset. After several years of receiving income and seeing the property grow in capital value, they determined they no longer needed the asset.

Their charitable adviser suggested that making an outright gift of the warehouse might allow them to make significant gifts to ministries they love and support. Ralph and Marge transferred their interest in the warehouse to a charitable foundation.

Ralph and Marge received a charitable tax deduction for the full appraised fair market value of the property. The property was sold, and Ralph and Marge instructed the charitable foundation to distribute the net proceeds to two of their favorite ministries who happily received the large cash distributions to further their work. Ralph and Marge enjoyed the satisfaction of excellent tax benefits and knowing they had made a lasting Kingdom impact with a gift of appreciated real estate.

Real estate gifts can be of houses, land, condominiums, vacation homes, commercial buildings, or most any type of real property. As with all non-cash gifts, tax rules vary by state and you should consult your own tax professionals before making a gift of real estate. If you are seeking to increase your generosity, and if you own real estate – the combination may be just right to accomplish your desires.

Commodities – The most common is a gift of grain from an active farmer.

Example: Ralph and Marge farm several hundred acres of cropland. Each year during the harvest they deliver one truckload of grain to their local elevator in the name of their favorite ministry. All the paperwork they receive when delivering this load shows the ministry as owner.

Once notified that they have a load of grain in their name, the ministry orders the elevator to sell at the current per bushel price. In a few days a check for the net value of the donated grain arrives at the ministry’s office. The cash gift is then put to work accomplishing the mission that Ralph and Marge so dearly love.

Though Ralph and Marge do not receive a charitable tax deduction for the gift of the load of grain – they do receive a kind letter of acknowledgement from the ministry leader. This confirms that the grain has been sold and that the ministry is putting the net proceeds of the sale to work accomplishing the mission.

In lieu of a charitable tax deduction, Ralph and Marge get to deduct the cost of producing the grain, and do not have to realize the taxable income that the sale of the grain would have produced. The net tax impact of their commodity gift is beneficial to them.

As with all gifts of non-cash assets, the tax rules are specific, and you should consult your own tax professionals before making a gift of any commodity.

Life Insurance – Policies can be gifted to the ministry or can name the ministry as a beneficiary.

Example: When their children were young, Ralph and Marge each purchased a life insurance policy naming the other as beneficiary. The thought was that if death occurred, the surviving spouse would need the additional income to care for the family. Now that their children are grown and no longer dependent up them, and because they have accumulated other assets, Ralph and Marge no longer need the policies.

In considering how they might increase their charitable giving to support their favorite ministry, Ralph and Marge learned that they could gift the policies outright to the ministry. Since each policy has a cash value, the ministry can choose to either hold the policies until death or surrender them and put the cash to work doing the mission today.

Ralph and Marge will receive a charitable tax deduction per the rules of life insurance contributions and know that they are making a significant gift to the ministry right now. If they choose, they can also make annual gifts of cash to the ministry that will be used to pay any ongoing premium – and receive further charitable tax deductions for the cash gifts.

If you have life insurance policies that are no longer needed for their original purpose – consider with your agent, the possibility of making a gift to ministry. You may find your policy is a perfect tool for increasing your generosity desires.

We have prepared a helpful eBook, A Steward’s Consideration of Life Insurance, which you can read or download here.

Conclusion (Creative Generosity Now)

When you desire to increase your generosity – consider “the other 90%” – your non-cash assets.

May we help? We have many resources available and can produce specific illustrations to explain how non-cash asset gifts can work for you.

Please contact us today!